Our Purpose

To provide expert loan portfolio risk management services that enable our customers to grow and thrive.

Risk Assessment

- Utilize our proprietary process to identify risks in credit quality.

- Expert process knowledge to enhance credit administration practices.

- Methodology designed to identify a shift in risk over time.

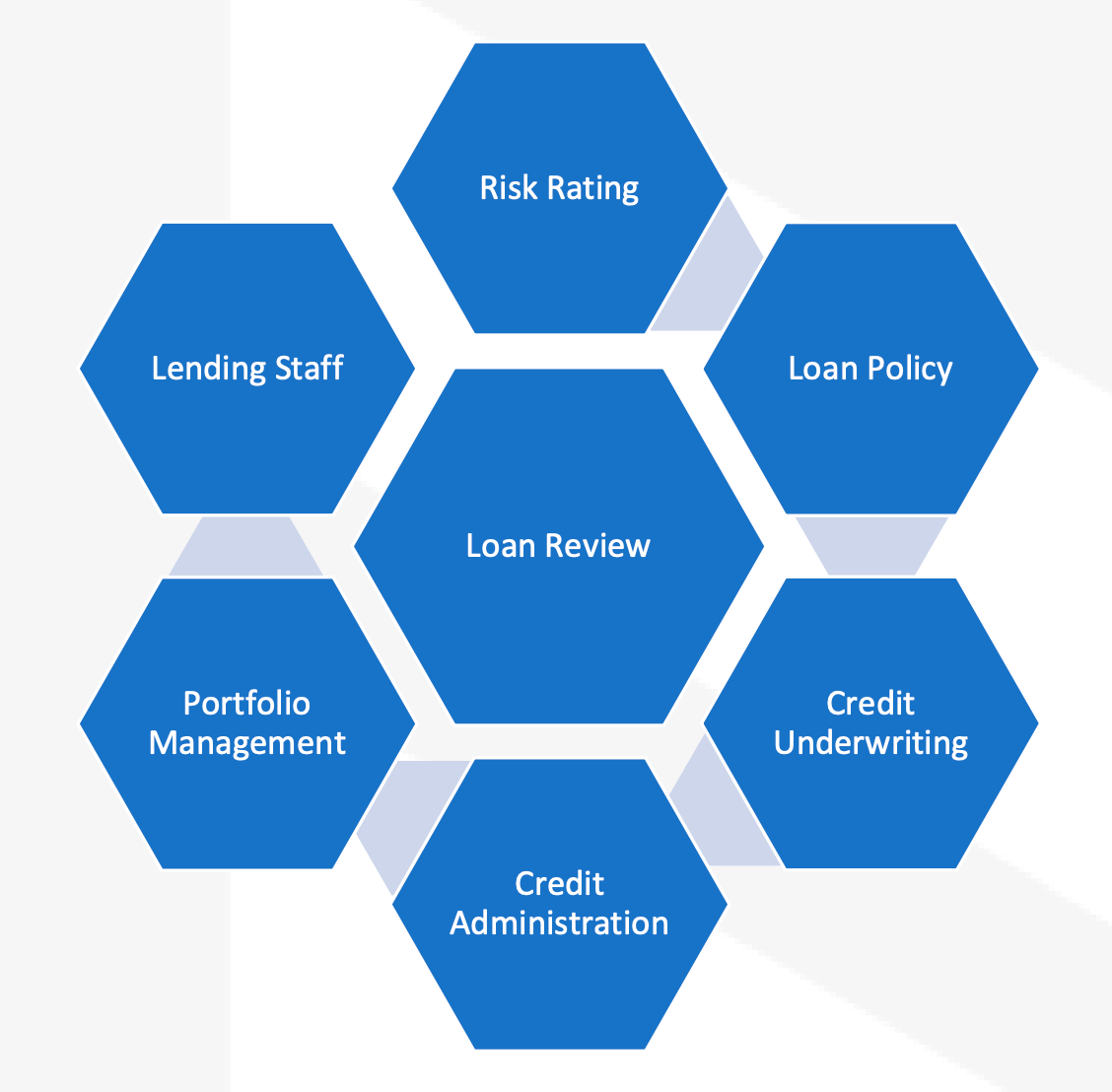

Our Services

We are a full-service provider of loan review and related services.

We work with you to understand your needs and serve as an independent extension of your credit risk management process.

Our Process

Our proprietary process provides insights into the effectiveness of the current loan grading process. Our independent Loan Review Services puts us in a unique position to gain perspective on the overall operational effectiveness of the credit department. Our experienced professionals provide insights into best practices to continue to enhance your risk management and credit department effectiveness.

Benefits of Working With Us

We bring the experience and discipline of a larger consulting firm with the direct interaction of Integrity ownership to deliver our services.

- Engagements designed to your specific requirements

- Partner with you to integrate our expertise into your risk management process

- Comprehensive and easy to read summary reporting

- Timely service and valuable advice at competitive rates

Why Choose Us?

Loan risk ratings are a critical part of our service, however we are much more than that. Our years of experience and current interactions with customers and regulators will deliver best practices and emerging trends to assure management of risk identification and mitigation. We utilize our proprietary risk management system to provide the confidence you need to foster profitable growth in your loan portfolio. Integrity’s methodology is straightforward yet customized. We are committed to providing the very best loan review and related services to you.